From Keytruda to Opdivo, blockbusters representing billions in annual revenue are about to face biosimilar competition. Here’s what’s coming, who’s most exposed, and how the industry is bracing for impact.

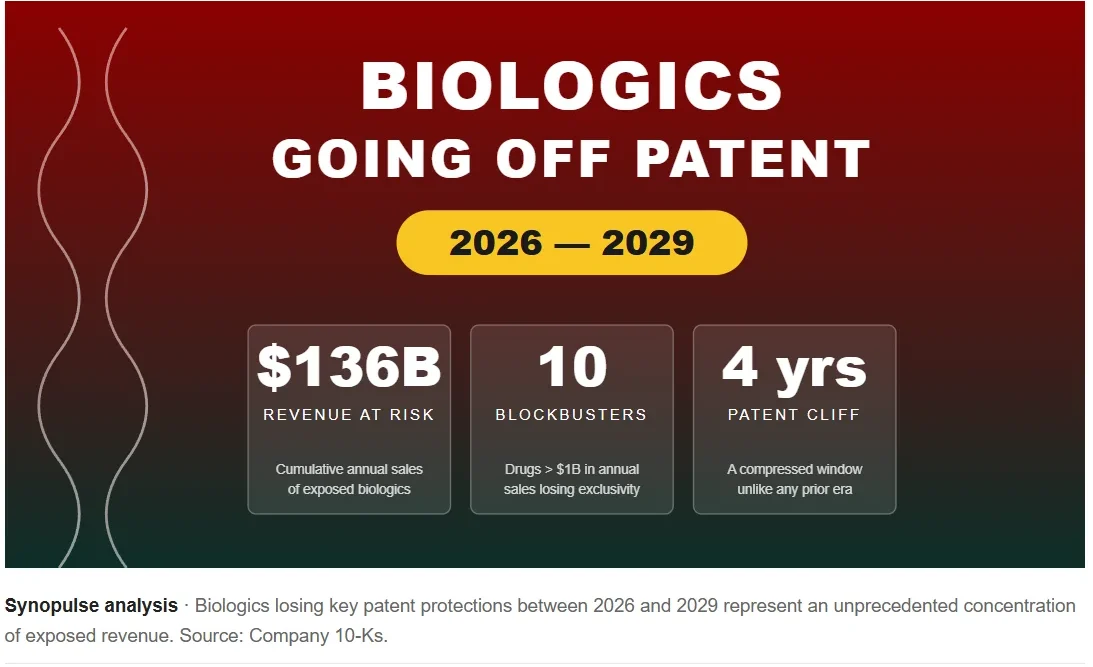

The biopharma industry has weathered patent cliffs before — but nothing quite like what’s unfolding between now and 2029. Over a four-year window, ten blockbuster biologics, including some of the best-selling drugs in pharmaceutical history, are losing core patent protection in major markets. The combined annual revenue at stake tops $136 billion, according to Synopulse’s analysis of company filings and third-party forecasts.

What makes this cliff different from the small-molecule washout of 2011-2014 isn’t just the dollar figure. It’s the molecules themselves. Antibody therapeutics, fusion proteins and complex glycosylated biologics don’t surrender market share as cleanly as oral generics. Biosimilar uptake has historically been slower, payers more conservative, and physicians more cautious. That dynamic is changing — fast.

Where the revenue actually sits

The headline number is $136 billion, but the curve is far from uniform. Roughly 73% of the at-risk revenue concentrates in 2028 and 2029, driven almost entirely by Keytruda and Opdivo — two checkpoint inhibitors that have redefined oncology and, between them, generate over $40 billion annually.

Revenue at risk by year of patent expiry

“We’re staring at an unusually back-loaded cliff,” said one industry analyst. “The first two years are manageable. 2028 is a stress test for the entire oncology business model.”

The class of 2026: The cliff begins

The opening salvo is already here. Kadcyla, a HER2-positive breast cancer mainstay, is losing its core U.S. patent protection this year, alongside Taltz for psoriasis and psoriatic arthritis. Lartruvo for soft tissue sarcoma rounds out the 2026 cohort.

Of these, Kadcyla is the headline event. With roughly $2.5 billion in 2025 sales, its erosion will be closely watched as a leading indicator for how aggressively biosimilar manufacturers pursue oncology biologics.

“Oncology biosimilars in the U.S. were a slow start. By 2026, slow is no longer the right word.” — Senior commercial lead, top-five biosimilar developer

2027: Diabetes and cardiology join the queue

The middle year of the cliff broadens the therapeutic exposure considerably. Trulicity, a GLP-1 that has been partially eclipsed by newer agents but still books over $7 billion annually, loses key formulation patents in 2027. Repatha, the PCSK9 inhibitor for hypercholesterolemia, follows the same year.

Rare disease, but still material

Don’t overlook the rare-disease franchises losing exclusivity in 2027. Myalept (lipodystrophy) and Sylvant (Castleman disease) generate modest absolute revenue but represent meaningful margin contributions for their owners — and rare-disease biosimilars remain a largely uncharted regulatory pathway.

The 2028 earthquake: Keytruda and Opdivo

Then comes 2028. Keytruda, on track to be the best-selling drug in pharmaceutical history before its expiry, faces biosimilar competition for the first time. Opdivo follows on a similar timeline. Together, the two PD-1 inhibitors generated roughly $37 billion in 2025.

Why 2028 matters

Keytruda alone represents approximately 46% of its originator’s pharmaceutical revenue. Even a 30% biosimilar erosion in year one would translate to a $7 billion top-line hole — an enormous gap to fill organically. Expect aggressive M&A activity in oncology and immunology between now and 2027 as originators race to diversify.Both originators have pursued mitigation strategies: a subcutaneous Keytruda formulation that may extend patent runway into the early 2030s, and investment in next-generation IO combinations and the LAG-3 franchise via Opdualag. Whether these tactics meaningfully slow biosimilar conversion is the multi-billion-dollar question.

2029: The closing wave

The cliff doesn’t end quietly. Darzalex (multiple myeloma), Ocrevus (multiple sclerosis) and Cosentyx (psoriasis, psoriatic arthritis) all face expiry in 2029, representing roughly $26 billion in additional exposed revenue.

Darzalex’s originator has been the most aggressive lifecycle manager of the three, transitioning a substantial portion of revenue to the subcutaneous Darzalex Faspro formulation, which carries differentiated patent protection. Industry observers expect Faspro to absorb 70-80% of legacy Darzalex revenue by the time biosimilars arrive — a textbook example of formulation-driven cliff mitigation.

The bottom line

The 2025-2029 biologics patent cliff is the largest concentrated loss of pharmaceutical exclusivity ever recorded. It will reshape the competitive landscape in oncology and immunology, accelerate biosimilar adoption in categories that have historically resisted it, and force a wave of M&A and pipeline reprioritization among originators.

The cliff has begun. The next five years will determine who climbs back up.